The Flight to Safety That Wasn’t Safe for Everyone

April 2026

TL;DR

· The dollar index surged above 100 for the first time since November, creating systematic headwinds for international equities and emerging markets.

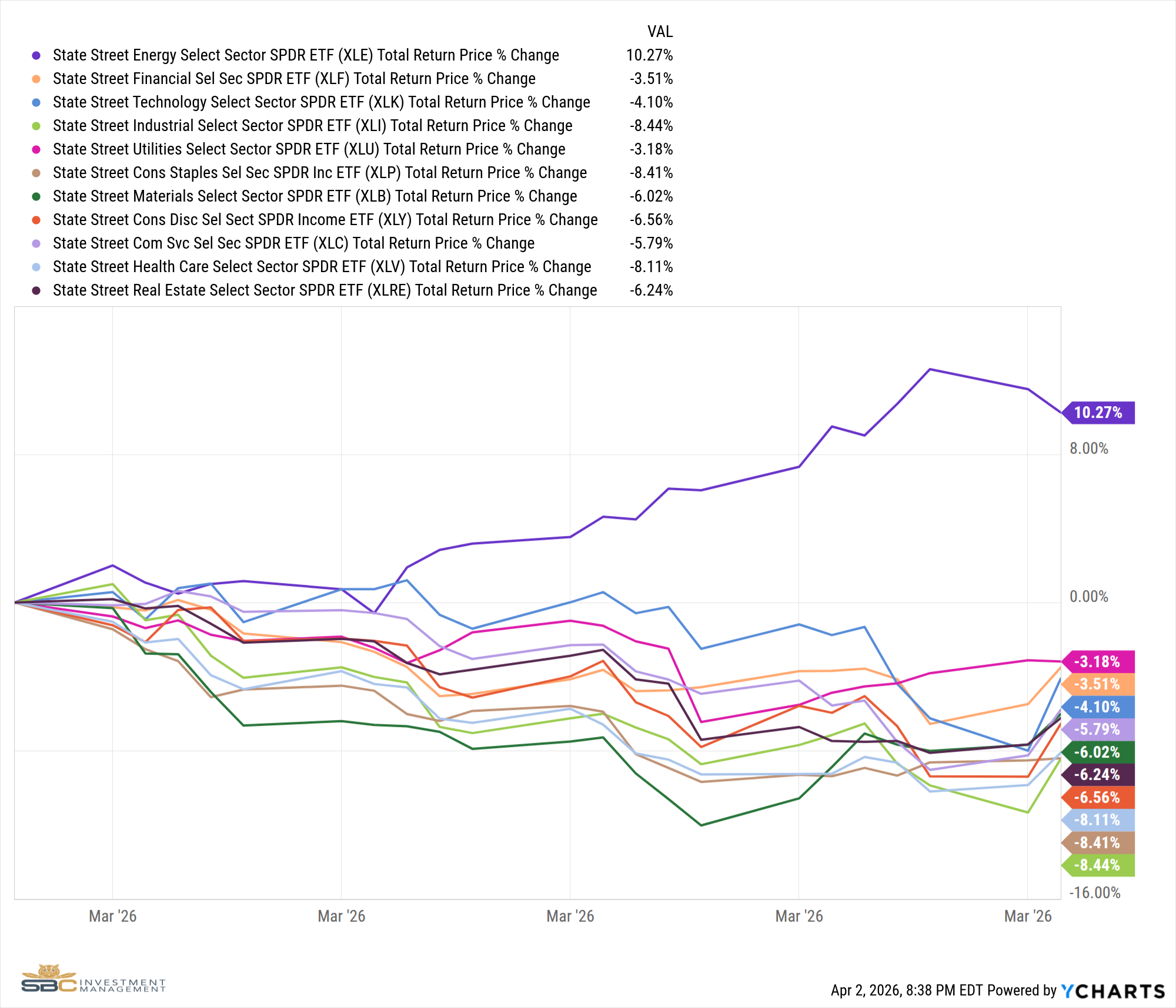

· Energy dramatically outperformed, with XLE up 10.27% in March as geopolitical tensions drove oil prices higher.

· We entered March with international exposure, absorbed early losses from the Iran conflict, and adapted, rotating into defensive sectors and adding to our energy exposures.

· Even our defensive pivots into real estate and long-term Treasuries faced headwinds as volatility spread across asset classes.

· Our willingness to adapt mid-month allowed us to slightly outperform benchmarks despite a -3.26% monthly return.

Flight to Safety, Flight from Everything Else

When uncertainty spikes, capital moves. It moves out of risk assets, out of foreign currencies, and into the perceived safety of the U.S. dollar. That’s not a new pattern, it’s one of the most consistent reflexes in global markets. March gave investors a live demonstration. The U.S.-Iran conflict triggered a swift flight to safety, and the dollar was the primary destination. The dollar index surged above 100 for the first time since November, and that single move set off a cascade of portfolio effects.

A stronger dollar mechanically reduces the value of foreign assets when translated back into U.S. terms, and it can pressure the fundamentals of international businesses that rely on dollar-denominated trade and financing. March was a clear example: the MSCI ACWI ex USA Index fell -10.71% while the S&P 500 declined -5.2%. When the dollar surges, international exposure can stop acting like diversification and start acting like a separate source of risk.

What made this particularly painful in the early weeks was that we entered March with meaningful international exposure, positions in India, Japan, Turkey, Mexico, and Israel that were part of a broader diversification thesis. When the attacks on Iran hit, those positions moved against us quickly. That loss was real, and it was ours to own. That said, most of these positions were meaningful contributors to performance coming into March. While the immediate drawdown was real, we were still realizing longer-term gains.

Taking the Hit, Then Adapting

We were fortunate that our process had us reducing risk and tilting toward energy in February, ahead of the geopolitical headlines. The Hedgeye GIP model was signaling a Quad 3 environment for March, characterized by decelerating growth alongside rising inflation, and that signal drove incremental defensive positioning before the month began. But reducing risk is not the same as eliminating it. We still carried both international and high-beta exposure into March, and the early days of the Iran conflict made that clear in a hurry.

What mattered after that was our response. We exited India, Mexico, Turkey, Japan, and emerging markets systematically as the dollar regime shift became undeniable. These weren’t panicked sells; they were disciplined acknowledgments that the macro backdrop had changed in a way that made those positions untenable. Exiting early in the month preserved enough capital to adapt for the weeks that followed.

The lesson isn’t that we timed the conflict, no one did. It’s that a repeatable process gave us a framework for responding when the unexpected happened. We knew what the regime called for. When the data confirmed the shift, we acted.

Even the Right Playbook Had Holes

After exiting international positions, we rotated further into what the Quad 3 playbook historically favors: energy through OIH and XOP, real estate through XLRE, long-term Treasuries through TLT, utilities through XLU, and gold through AAAU. The logic was sound. The results were mixed.

Real estate, Treasuries, and even gold struggled. As Treasury yields climbed, the 10-year moved from 3.97% to 4.30% over the course of the month, rate-sensitive assets that normally hold up in slower-growth environments came under pressure instead. Volatility didn’t stay contained to equities, it spread. The VIX closed the month above 30, and the usual diversifiers simply didn’t diversify. When correlations converge across asset classes like that, there are very few places to hide.

There was only one GICS sector that was safe in March: energy. XLE gained ground while nearly every other major sector declined.

Our initial energy exposure through OIH and XOP helped soften the blow early in the month. As conviction in the regime grew, we added AMLP and NORW late in March to deepen that positioning. The process flagged Quad 3 in February; the Iran conflict simply confirmed what the data was already beginning to tell us.

Geography Matters When Currency Moves This Fast

The international experience in March deserves its own examination. We held positions across Japan, India, Turkey, Mexico, and Israel coming into the month. Each faced compounding pressure, first from the geopolitical shock, then from the dollar’s sustained move higher. Emerging markets declined broadly, as their currencies weakened sharply against the dollar.

The only international position we added during the month was Norway, which benefits from energy production and tends to strengthen when commodity prices rise. That allocation worked precisely because the same currency dynamics that hurt other regions helped it. The contrast was instructive: in a dollar surge, geography becomes a currency trade whether you intend it to be or not.

What March Taught Us About Portfolio Construction

March reminded us that diversification benefits can disappear when correlations converge. Bonds didn’t offset equity losses. International stocks amplified them. Even assets with strong historical precedent in the prevailing regime, real estate, healthcare, and gold, struggled when yield volatility overwhelmed the usual relationships. The only refuge was energy, and getting there required moving through pain first.

That’s the honest account of the month. We came in with exposure, absorbed early losses, adapted our positioning, and still finished the month slightly ahead of benchmarks that fell harder and faster. The process didn’t protect us from every loss; it gave us the discipline to limit them and the framework to respond as conditions shifted.

Looking forward, the dollar’s move above 100 establishes a new baseline. International allocations face structural headwinds until currency trends reverse. Commodity and energy exposures remain attractive as inflation proves stickier than consensus expects. And March reinforces something we return to often: in volatile regimes, the goal isn’t to be right about everything. It’s to be wrong in ways you can recover from, and right about the things that matter most.

Model Performance Update

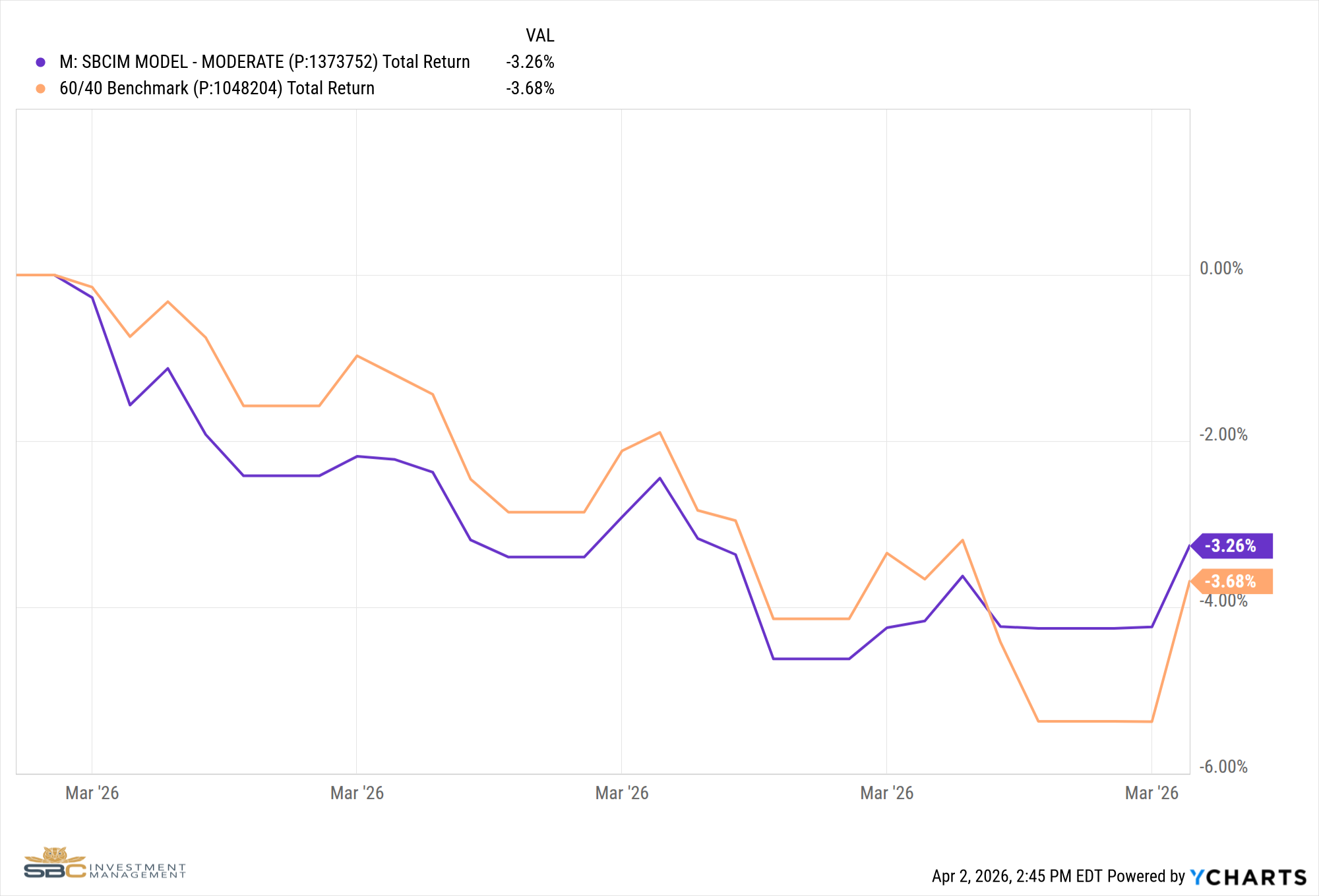

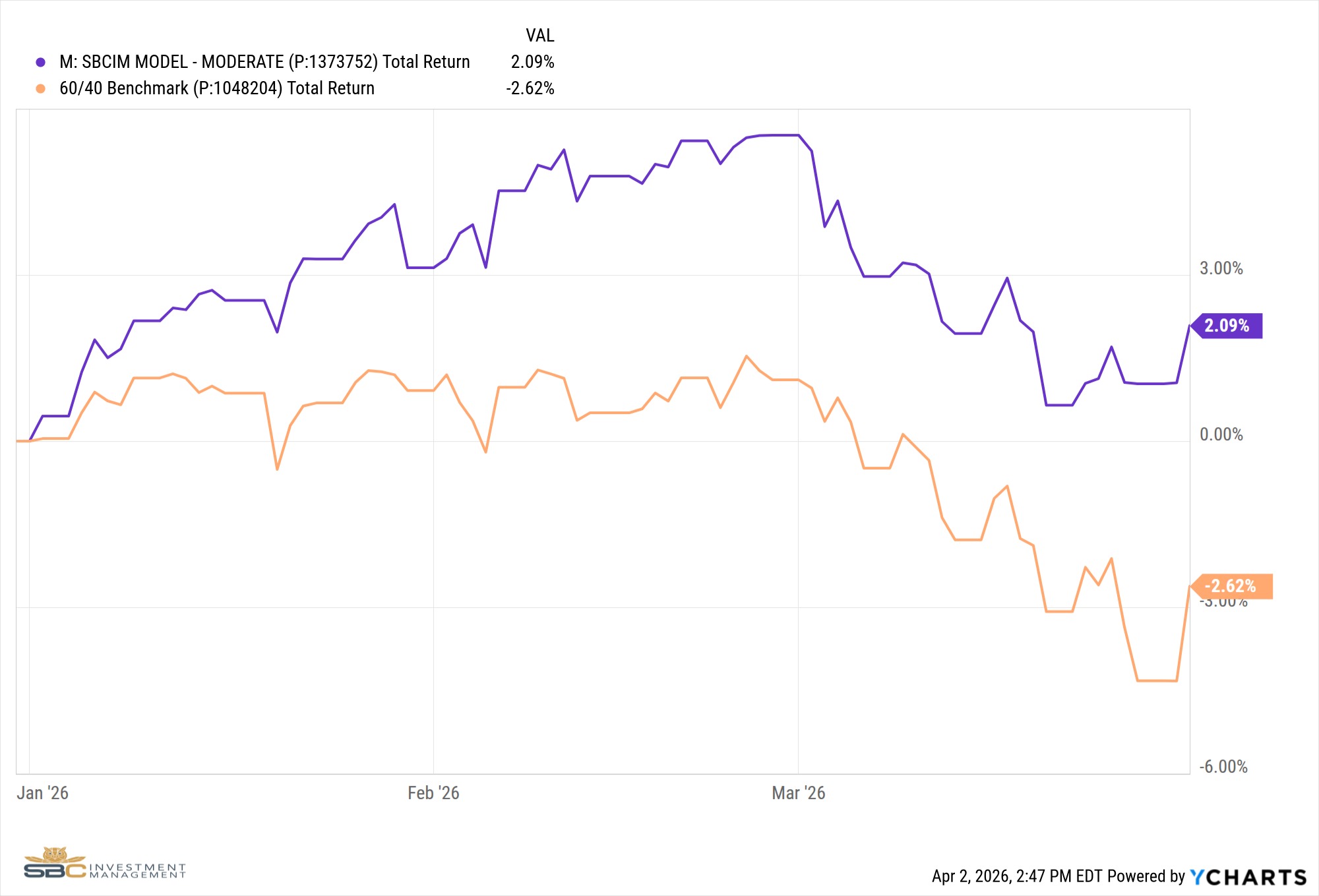

Our Moderate Model Portfolio returned -3.26% during the month of March and has returned 2.09% YTD.

Changes to the Model Portfolio in March

Date: March 2, 2026

· Replaced CLOZ (AAA CLOs) with TLT (long-term Treasuries) in Satellite 2.

· Added XLB (Materials) in Satellite 1 using excess cash.

Date: March 3, 2026

· Sold INDA (India) and ITB (home construction) in Satellite 1, replaced with XLU (Utilities).

· Sold FXC (Canadian dollar) in Satellite 3.

· Removed HYG (High Yield) in Satellite 2, added to TLT (Long-term Treasuries) and LQD (Investment-grade bonds).

Date: March 6, 2026

· Sold IWM (Small caps), XLB (Materials), and TUR (Turkey) in Satellite 1.

· Added XLRE (Real Estate) in Satellite 1.

Date: March 9, 2026

· Sold EEM (Emerging Markets), JPXN (Japan), and EWW (Mexico) in Satellite 1.

· Added OIH (oil services) while increasing exposure to XLU (utilities) and XLRE (real estate) in Satellite 1.

· Added to AAAU (gold) in Satellite 3.

Date: March 24, 2026

· Removed XLI (industrials) and XLRE (real estate) in Satellite 1.

· Added AMLP (MLPs) and NORW (Norway) to Satellite 1.

· Moved the 4% cash position from Satellite 1 to Satellite 3.

· Added COM (commodities) to Satellite 3.

Date: March 27, 2026

· Removed EIS (Israel), added XTL (Telecoms) in Satellite 1.

Date: March 30, 2026

· Swapped CPB (Campbell’s Soup) for SFD (Smithfield Foods) in Satellite 4.

March Performance with Benchmark

YTD Performance with Benchmark

If you have any questions about the above, please reach out to schedule a one-on-one meeting so we can review your situation.

Sincerely,

Bryant Andrus, MSF, CFP®

President

SBC Investment Management

P: (602) 641-5996

M: (319) 520-2033

E: bandrus@sbcinvestmentmanagement.com

Jake Rehkop

Investment Analyst, Junior Portfolio Manager

SBC Investment Management

P: (435) 775-2950

M: (435) 590-8317